Desplácese hacia abajo para leer esto en español.

Honoring the Amazing Fathers in our Lives!

I’m so excited to celebrate my husband this weekend! He is an incredible father! As you can see in the photo, he gets on rides that spin at Disneyland to make the kids and I happy, even though he hates rides that spin – that is love 😂 In seriousness, my husband is a great father for so many reasons. He is so sacrificial and he does so much for our kids. He cooks, goes to the market, drives them all around town… while also wearing many hats at the office. To my husband, my father, and all the fathers and father-figures out there, we honor you and deeply appreciate the impact you have on our lives. Your guidance and strength truly shape us into who we are. Wishing you all a very Happy Father’s Day!

A Personal Note from Alex

If you worry about your financial situation, you are far from alone. Americans’ financial concerns have increased in recent years and are at levels not seen in more than a decade.

Seventy-seven percent of Americans are anxious about their financial situation, according to a Capital One survey. The survey also found that “bigger picture” thinking about long-term goals can lead to healthier financial behaviors and less stress. For many, their long-term financial goals amount to having enough money to retire. But most Americans do not have a plan for their money and property beyond their own lifetime. Only 32 percent of Americans have an estate plan that describes a distribution path for their assets.

The basic function of an estate plan is to make your intentions known about who should receive your money and property upon your death and how you want them to receive it. Not having an estate plan or having an outdated estate plan means that state law and the courts may have to make those decisions for you. And what they decide could be very different from what you would choose.

For example, depending on what state you live in, default succession law could divide your money and property among your surviving spouse and children. But maybe you want everything to go outright to your spouse to ensure that they are taken care of. Maybe you are in a second marriage and would like a larger percentage or all of your estate to go to your children.

Or perhaps you want to place conditions on a child’s inheritance because they are a minor, have demonstrated poor money habits, could get divorced (leaving some of your hard-earned money and property in the hands of their ex-spouse), or are receiving government benefits that may be impacted by an inheritance. Also, with an estate plan, you are able to leave gifts or funds to grandchildren, other relatives, life partners, friends, or charities that may not otherwise be considered when a judge looks to the state law.

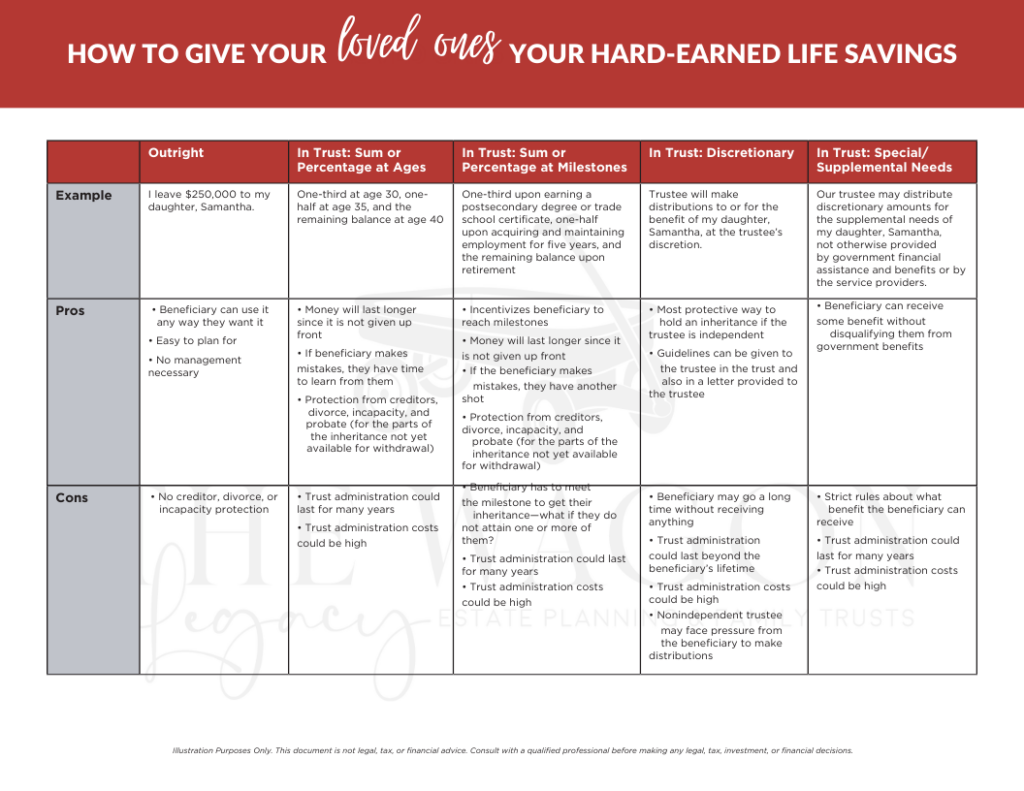

If you want to take charge of who gets your money and property upon your passing and in what amounts, you need to make an estate plan. It could be as simple as a will that outlines specific gifts to certain beneficiaries. Or you can engage in trust-based planning by placing money and property in a trust for beneficiaries so that inheritances can be managed and distributed on their behalf based on your preferences.

Trusts are almost infinitely customizable and can be included as part of your will or can be drafted as a separate tool. You can stipulate that a beneficiary will receive a sum or percentage of their inheritance at certain ages, upon reaching a milestone, or for defined events or purchases, or you can even give a trustee full discretion to distribute trust funds when or how they deem to be in the best interest of the beneficiary.

In addition to leaving money and property to loved ones, you might want to make a charitable donation as part of your legacy. The only way to fully express your wishes in this regard is through an estate plan. There is no default state law for charitable gifts when somebody dies without a will.

More than two-thirds of Americans told Caring.com that having a will is important—yet fewer than one-third have one. The reasons given by respondents reflect a lack of understanding about what an estate plan is and why it is important:

1 — If you put off creating an estate plan until you have medical problems, you could become mentally unable to make a will or establish other important documents. Everyone, no matter their financial situation, should have an estate plan.

2 — Estate planning can be particularly important for high-net-worth individuals to minimize taxes and preserve wealth. But if you own anything of value, have loved ones to take care of, or want to provide a smooth and easy transition for your family members if you become unable to make financial or medical decisions for yourself, then having a plan in place is a must.

3 — Even if you do not have a spouse or minor children, there is surely somebody—or some charitable cause—that you care about who would benefit from a gift. Without an estate plan, these individuals or charities may receive nothing.

4 — Estate plans should generally be revisited and updated every few years to reflect major life events or changes in circumstances, either in your life or in the lives of your beneficiaries to ensure that your documents still reflect your wishes.

We understand that contemplating your mortality and what happens to your stuff after you die can be uncomfortable. But engaging in thoughtful estate planning can help you take control and eliminate some of the stress and uncertainty that accompanies these topics.

Whether you have yet to start an estate plan, have stalled in the planning process, or need to update an existing plan, we are here to help. Please get in touch and let us know how we can assist you with a plan that secures the legacy you hope to leave.

Don’t Let This Crucial Question Derail Your Estate Plan

Crafting or updating your estate plan can feel daunting. Not only are you striving to cover all bases, but it’s also an emotionally heavy process. Preparing for the inevitable absence requires diligence and sensitivity. Amidst the challenges, it’s common to overlook two crucial inquiries: who inherits your possessions and how you wish for them to be distributed, whether to individuals or charities.

In today’s blog post, I highlight the significance of addressing these questions and providing precise instructions for your beneficiaries. Various circumstances may influence these decisions, emphasizing the importance of understanding your options and incorporating detailed directives into your estate plan.

Lee esto en Español:

¡Honrando a los padres asombrosos en nuestras vidas!

¡Estoy muy emocionada de celebrar a mi esposo este fin de semana! ¡Es un padre increíble! Como puedes ver en la foto, se sube a las atracciones que giran en Disneyland para hacernos felices a los niños y a mí, aunque odia las atracciones que giran; eso es amor 😂 En serio, mi esposo es un gran padre por muchas razones. Es muy sacrificado y hace mucho por nuestros hijos. Cocina, va al mercado, los lleva por toda la ciudad… y al mismo tiempo desempeña muchas funciones en la oficina. A mi esposo, mi padre y todos los padres y figuras paternas, los honramos y apreciamos profundamente el impacto que tienen en nuestras vidas. Tu guía y fortaleza realmente nos convierten en quienes somos. ¡Les deseo a todos un muy Feliz Día del Padre!

Una nota personal de Alex

Si le preocupa su situación financiera, no está ni mucho menos solo. Las preocupaciones financieras de los estadounidenses han aumentado en los últimos años y se encuentran en niveles no vistos en más de una década.

Según una encuesta de Capital One, el setenta y siete por ciento de los estadounidenses están ansiosos por su situación financiera. La encuesta también encontró que pensar en un “panorama más amplio” sobre objetivos a largo plazo puede conducir a comportamientos financieros más saludables y menos estrés. Para muchos, sus objetivos financieros a largo plazo equivalen a tener suficiente dinero para jubilarse. Pero la mayoría de los estadounidenses no tienen un plan para su dinero y sus propiedades más allá de su propia vida. Sólo el 32 por ciento de los estadounidenses tiene un plan patrimonial que describe una ruta de distribución de sus activos.

La función básica de un plan patrimonial es dar a conocer sus intenciones sobre quién debe recibir su dinero y sus bienes tras su muerte y cómo desea que los reciban. No tener un plan patrimonial o tener un plan patrimonial desactualizado significa que es posible que la ley estatal y los tribunales tengan que tomar esas decisiones por usted. Y lo que ellos decidan podría ser muy diferente de lo que usted elegiría.

Por ejemplo, dependiendo del estado en el que viva, la ley de sucesión predeterminada podría dividir su dinero y sus bienes entre su cónyuge e hijos sobrevivientes. Pero tal vez usted quiera que todo le llegue directamente a su cónyuge para asegurarse de que sea atendido. Tal vez esté en un segundo matrimonio y le gustaría que un porcentaje mayor o la totalidad de su patrimonio vaya a sus hijos.

O tal vez desee imponer condiciones a la herencia de un hijo porque es menor de edad, ha demostrado malos hábitos económicos, podría divorciarse (dejando parte del dinero y propiedades que ganó con tanto esfuerzo en manos de su excónyuge) o está recibiendo Beneficios gubernamentales que pueden verse afectados por una herencia. Además, con un plan patrimonial, puede dejar obsequios o fondos a nietos, otros parientes, compañeros de vida, amigos o organizaciones benéficas que de otro modo no podrían considerarse cuando un juez examina la ley estatal.

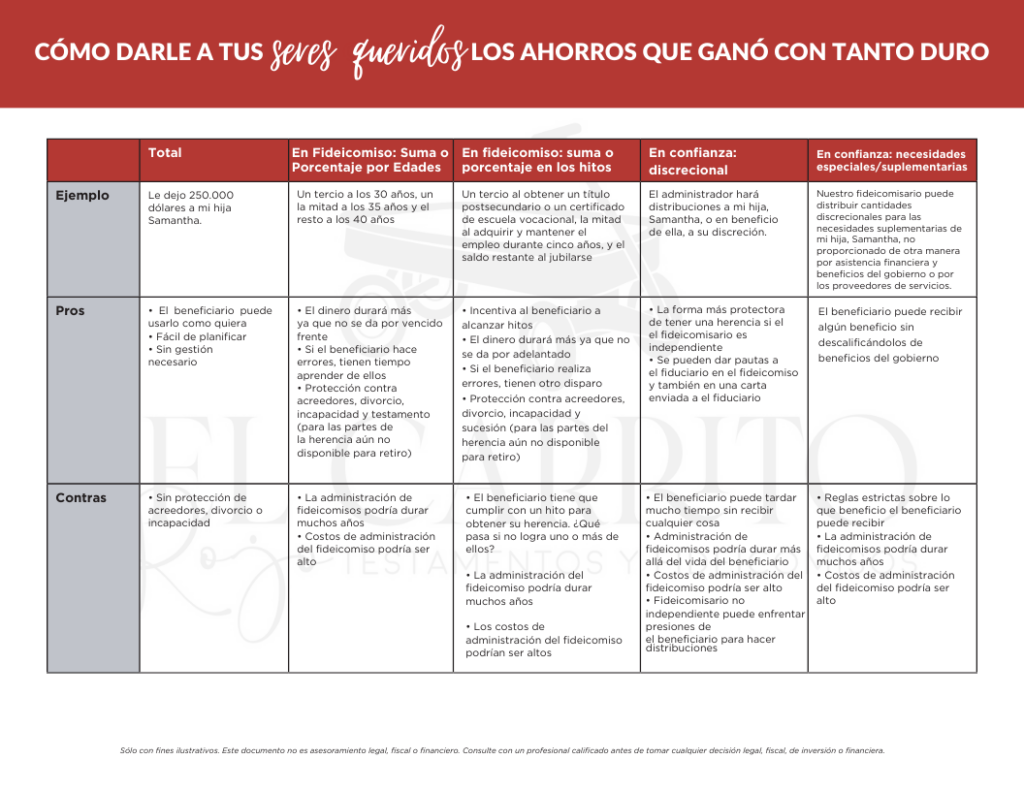

Si desea hacerse cargo de quién recibe su dinero y sus propiedades cuando usted fallece y en qué cantidades, debe elaborar un plan patrimonial. Podría ser tan simple como un testamento que describa obsequios específicos para ciertos beneficiarios. O puede participar en una planificación basada en fideicomisos colocando dinero y propiedades en un fideicomiso para los beneficiarios, de modo que las herencias puedan administrarse y distribuirse en su nombre según sus preferencias.

Los fideicomisos son casi infinitamente personalizables y pueden incluirse como parte de su testamento o pueden redactarse como una herramienta separada. Puede estipular que un beneficiario recibirá una suma o porcentaje de su herencia a determinadas edades, al alcanzar un hito, o para eventos o compras definidas, o incluso puede darle a un fideicomisario total discreción para distribuir los fondos fiduciarios cuando o como lo considere oportuno. sea en el mejor interés del beneficiario.

Además de dejar dinero y propiedades a sus seres queridos, es posible que desee hacer una donación caritativa como parte de su legado. La única manera de expresar plenamente sus deseos a este respecto es a través de un plan patrimonial. No existe una ley estatal predeterminada para las donaciones caritativas cuando alguien muere sin testamento.

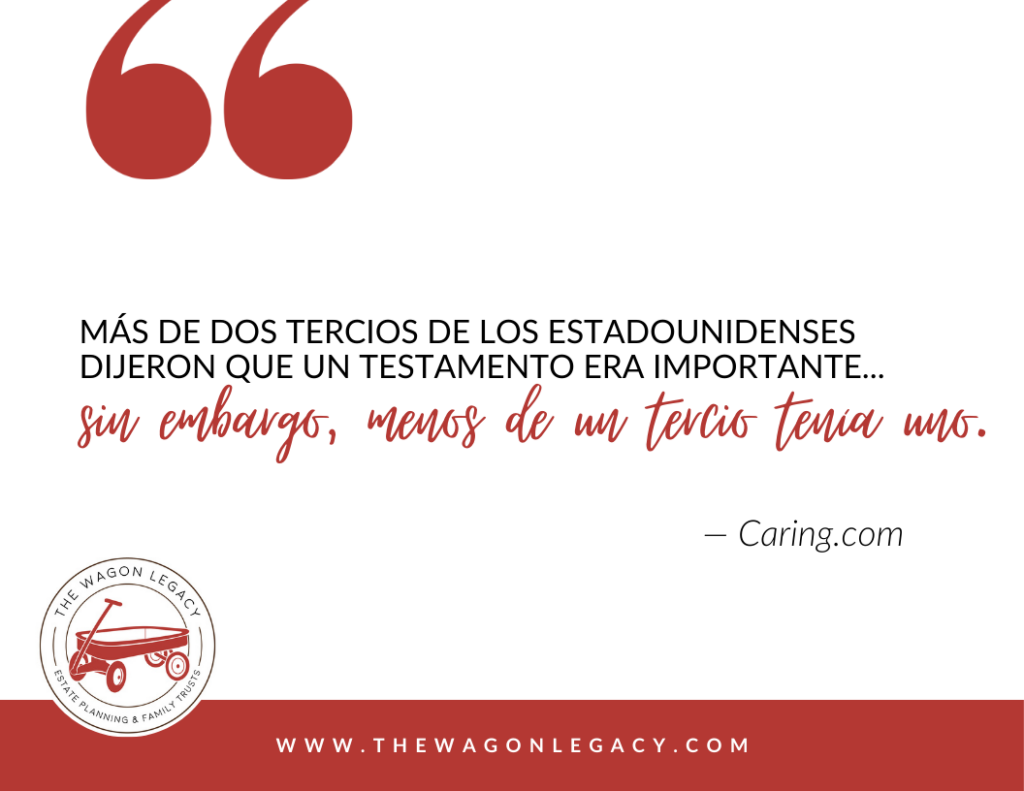

Más de dos tercios de los estadounidenses dijeron a Caring.com que tener un testamento es importante; sin embargo, menos de un tercio lo tiene. Las razones dadas por los encuestados reflejan una falta de comprensión sobre qué es un plan patrimonial y por qué es importante:

1 — Si pospone la creación de un plan patrimonial hasta que tenga problemas médicos, podría quedar mentalmente incapaz de hacer un testamento o establecer otros documentos importantes. Todo el mundo, sin importar su situación financiera, debería tener un plan patrimonial.

2 — La planificación patrimonial puede ser particularmente importante para las personas con alto patrimonio neto para minimizar los impuestos y preservar la riqueza. Pero si posee algo de valor, tiene seres queridos que cuidar o desea brindar una transición fácil y sin contratiempos a los miembros de su familia si no puede tomar decisiones financieras o médicas por sí mismo, entonces contar con un plan es una debe.

3 — Incluso si no tienes cónyuge ni hijos menores, seguramente hay alguien (o alguna causa benéfica) que te importa y que se beneficiaría de un regalo. Sin un plan patrimonial, es posible que estas personas o organizaciones benéficas no reciban nada.

4 — Los planes patrimoniales generalmente deben revisarse y actualizarse cada pocos años para reflejar eventos importantes de la vida o cambios en las circunstancias, ya sea en su vida o en la vida de sus beneficiarios, para garantizar que sus documentos aún reflejen sus deseos.

Entendemos que contemplar su mortalidad y lo que sucede con sus cosas después de su muerte puede resultar incómodo. Pero participar en una planificación patrimonial bien pensada puede ayudarle a tomar el control y eliminar parte del estrés y la incertidumbre que acompañan a estos temas.

Ya sea que aún no haya iniciado un plan patrimonial, se haya estancado en el proceso de planificación o necesite actualizar un plan existente, estamos aquí para ayudarlo. Póngase en contacto y háganos saber cómo podemos ayudarlo con un plan que asegure el legado que espera dejar.

No permita que esta pregunta crucial descarrile su plan patrimonial

Elaborar o actualizar su plan patrimonial puede resultar abrumador. No sólo te esfuerzas por cubrir todas las bases, sino que también es un proceso emocionalmente pesado. Prepararse para la inevitable ausencia requiere diligencia y sensibilidad. En medio de los desafíos, es común pasar por alto dos cuestiones cruciales: quién hereda sus posesiones y cómo desea que se distribuyan, ya sea a individuos o a organizaciones benéficas.

En la publicación del blog de hoy, destaco la importancia de abordar estas preguntas y brindar instrucciones precisas a sus beneficiarios. Varias circunstancias pueden influir en estas decisiones, lo que enfatiza la importancia de comprender sus opciones e incorporar directivas detalladas en su plan patrimonial.